Weekly Macro Report

Macro Brief — May 12, 2026

Oil’s $99.64 creep warns late-cycle tightening is taking the wheel from earnings euphoria.

Parson Tang — May 12, 2026Powered by MARY

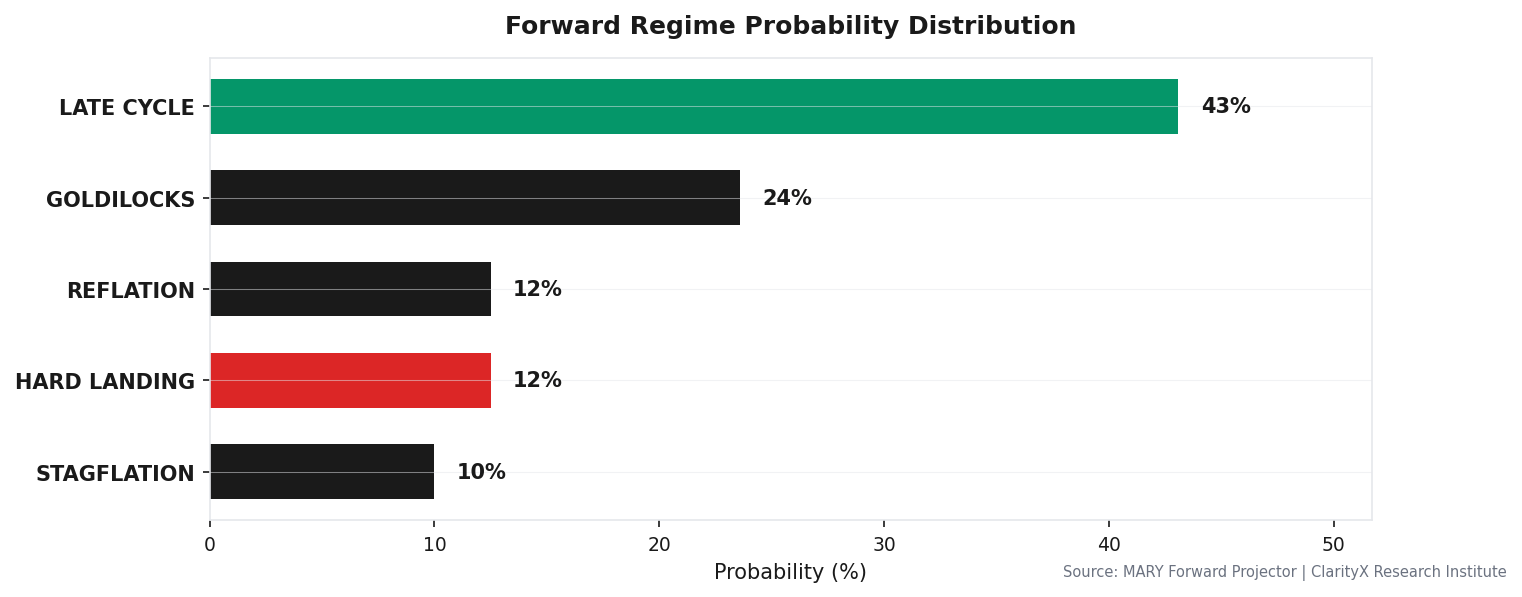

The picture is largely unchanged from last week, but oil creeping toward $100 is the variable that demands attention. WTI settled at $99.64, up $1.73 from last week, and now sits just $1.57 below the $98.07 level I flagged as the margin-squeeze tripwire. The regime remains LATE_CYCLE with 43% confidence — unchanged — but the forward risk is ELEVATED, and I am acting on that assessment. Two critical trip wires are live (NFCI and HY OAS), triggering an 18% defensive shift. This is not a call to panic; it is a call to be positioned for a regime flip on the next data point.

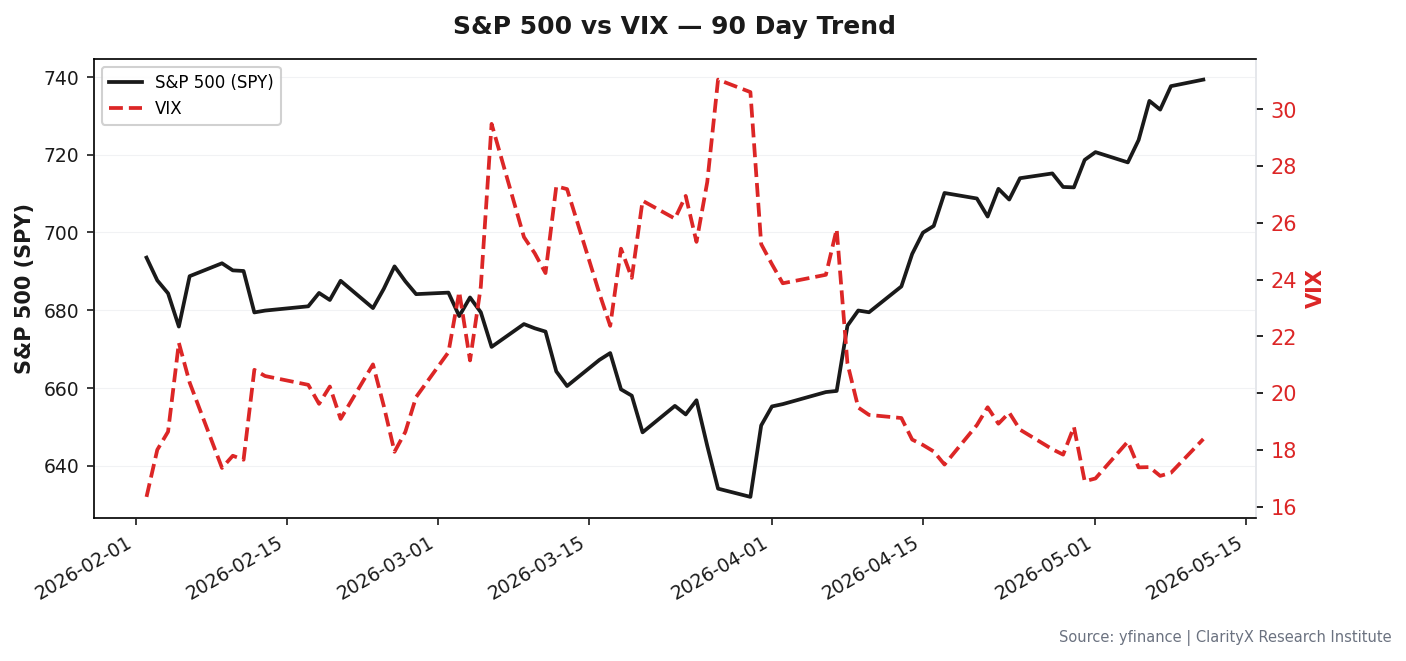

S&P 500 vs VIX — 90 Day Trend

S&P 500 vs VIX — 90 Day Trend

The core tension is straightforward. Wage growth held at 3.52%, which is sticky enough to keep the Fed on hold, while CPI at 3.32% YoY means realized inflation is not cooperating with the 2.45% forward expectation that markets have priced in. The Michigan 5-year expectation at 3.4% is consistent, but the gap between realized CPI and forward expectations is the fault line. If oil breaks $100 and stays there, that gap widens — and the Fed's inability to ease becomes a binding constraint on equity multiples. The LEI is expanding at 56.36% YoY, which argues against recession, but the GDP signal is weak at 0.5% QoQ SAAR. Growth is slowing, not collapsing. That is the definition of late cycle.

Credit spreads tightened slightly to 0.99%, which is the only reason the equity allocation is still at 61%. The investment-grade credit spread (Baa-10Y) at 0.99% is not signaling stress, but the second critical trip wire — NFCI — is. I do not publish the NFCI value here, but I will say this: when two critical wires are live, the model is telling me that the transmission mechanism from oil to credit to equity is under watch. The VIX at 17.08 is benign, but that is a lagging indicator. The VIX will not spike until the market is already repricing. By then, the allocation shift is too late.

I was wrong last week about the pace of oil's move. I expected $98 to be tested within days, not weeks. The market absorbed the Hormuz closure risk with surprising calm, and the earnings tailwind on May 11 provided a bid that kept equities supported. That bid is real — Q1 earnings were solid — but earnings do not insulate against a margin squeeze when input costs rise and the Fed cannot cut. The question is not whether the squeeze happens; it is whether oil stays above $98 long enough for it to show up in Q2 guidance. That is the next catalyst.

Forward Regime Probability Distribution

Forward Regime Probability Distribution

What Would Change My Mind

I will reduce equity to 50% and raise cash to 20% if WTI closes above $105 for two consecutive weeks. That is the level where wage growth at 3.52% becomes a margin-killer, not a headwind.

I will cut equity to 45% and add duration if weekly jobless claims break above 236,500. That is the engine's threshold for labor market deterioration, and it is the fastest way the late-cycle regime flips to contraction.

I will add back the 18% defensive shift — fully restoring equity — if the HY OAS tightens below 0.85% and NFCI returns to neutral. That would mean credit markets are disagreeing with the oil signal, and I will trust the credit market over the commodity market every time.

Levels that matter: WTI $99.64 · HY OAS 0.99% · 10Y real yield 2.3% · Weekly jobless claims 236,500 · VIX 17.08

For the full signal dashboard, allocation table, and watch list, see this week's CIO Weekly →

Get this research delivered

New analysis, directly to your inbox. Research notifications only.