Weekly Macro Report

Macro Brief — May 05, 2026

Stocks just matched a 156-year rarity—and the last three times ended in recession.

Parson Tang — May 5, 2026Powered by MARY

The stock market is doing something for only the 4th time in 156 years, and history is very clear about what happens next — but this time feels different because the regime signal itself is unclear, not the direction.

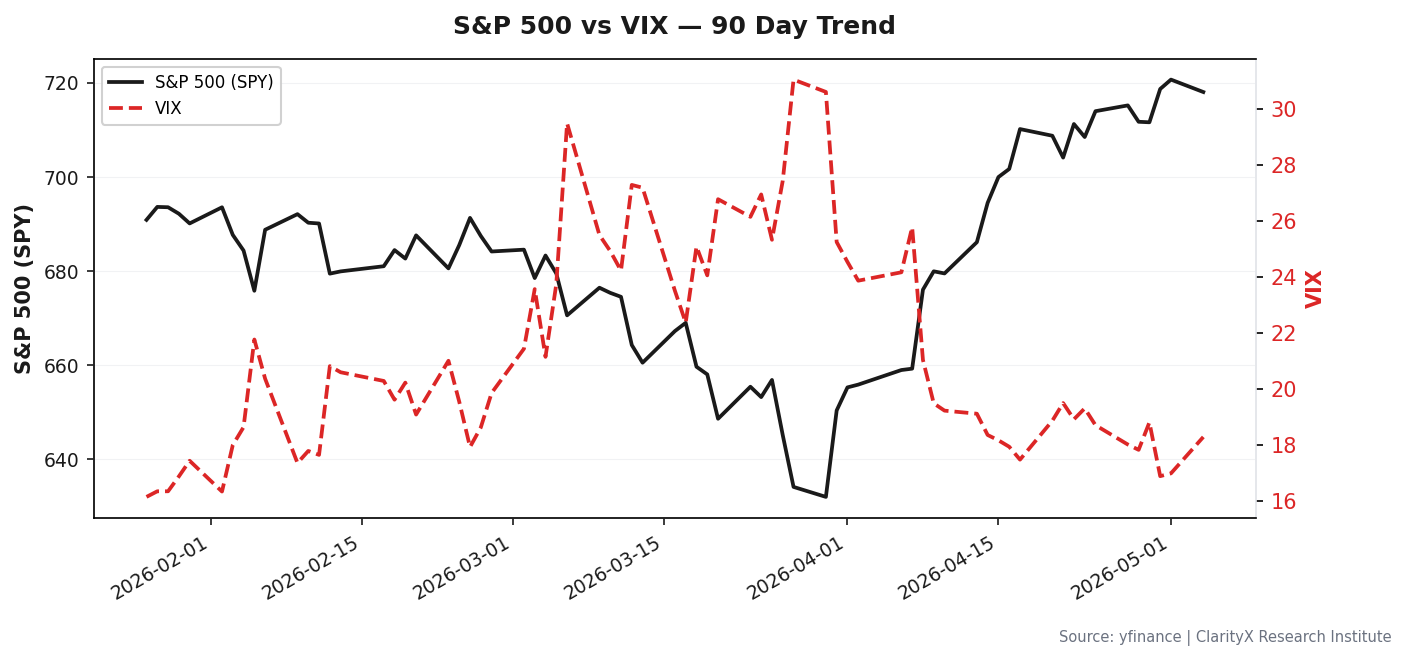

S&P 500 vs VIX — 90 Day Trend

S&P 500 vs VIX — 90 Day Trend

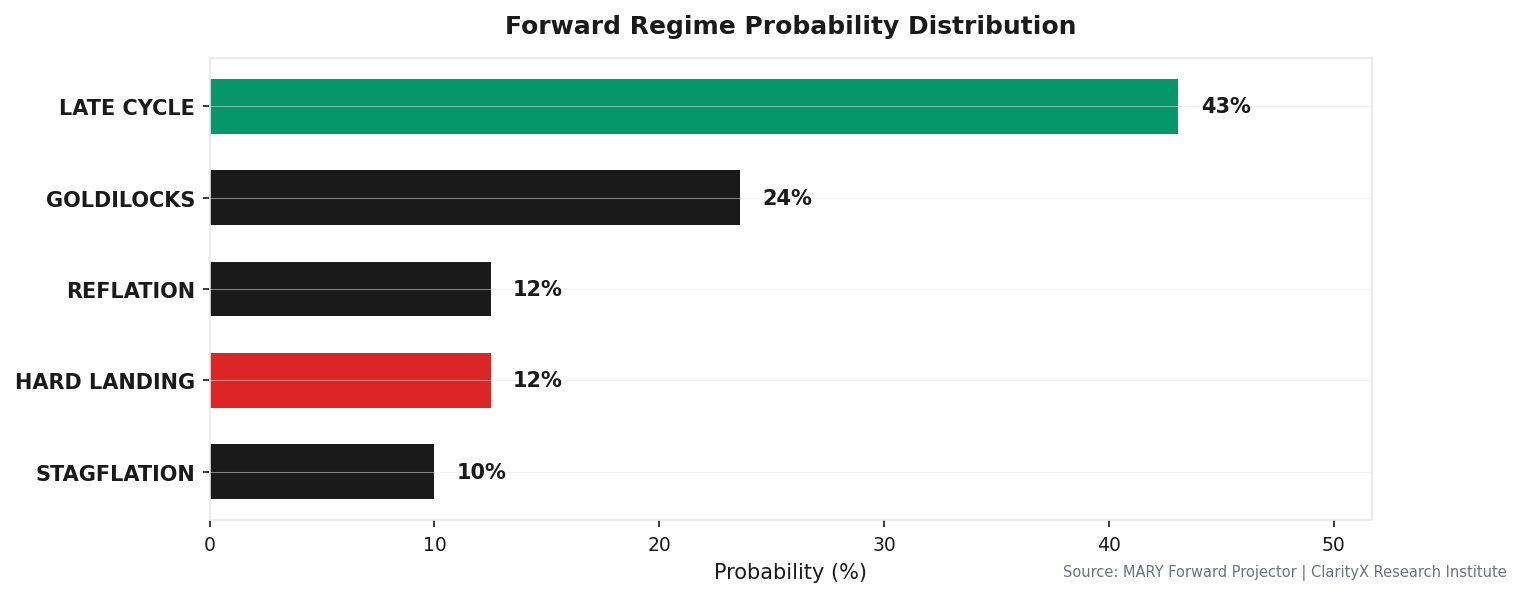

Confidence in the Late-Cycle label sits at 43%, essentially flat from 46% two weeks ago. That is the most important number in this brief. When confidence is below 50%, the right posture is preparation, not prediction. The engine is telling me the base case could flip on one data print, and the forward risk summary confirms it — 24% probability of a transition to Goldilocks in 3-6 months, but one critical trip wire (High-Yield OAS) is already active, forcing a 9% defensive shift. The market is pricing perfection in equities while the bond market is pricing hesitation. That divergence is not sustainable.

Let me be honest about where last week's call was wrong. I framed the recession regime as the base case, with oil at $104 and the 10-year real yield at 2.3% acting as a restrictive anchor. The engine has since reassessed. The yield curve is now 1.2 standard deviations above its average, which is a genuinely bullish signal. The LEI is expanding at 56.36% YoY — that is not a recessionary profile. I leaned too hard into the oil shock narrative and underestimated the curve's predictive power. The correction is baked into the 43% confidence number. I am not ignoring it.

The transmission mechanism this week runs through sector rotation. Energy (XLE) is leading at +17.1% over three months, which makes sense with WTI at $104.28. Technology (XLK) is also leading at +12.77%, which does not make sense in a recessionary frame but fits perfectly in a late-cycle Goldilocks transition. Utilities (XLU) at +7.96% is the tell — defensive leadership without panic. The sector rotation signal is flashing DEFENSIVE ROTATION (WARNING), but the character is orderly, not chaotic. The VIX at 16.99 confirms that. There is no fear capitulation. There is a quiet repositioning happening beneath the surface.

The leveraged ETF narrative — three areas up at least 150% in April — is the canary. When retail is levered into momentum and the forward risk is elevated, the drawdown potential compounds faster than the upside. I am not shorting momentum, but I am not adding to it either. The 9% defensive shift is already in place. If the trip wire on High-Yield OAS triggers again, that number goes higher.

Forward Regime Probability Distribution

Forward Regime Probability Distribution

What Would Change My Mind:

-

If High-Yield OAS breaks above 5.0% — that is the single credit stress threshold the engine monitors. If it crosses, I will increase the defensive shift from 9% to 15% and reduce equity exposure by an additional 5% into cash. Credit is the transmission mechanism between financial conditions and the real economy. When it breaks, the regime flips.

-

If weekly jobless claims exceed 236,500 — this is the labor market trip wire. Claims are the most real-time, least revised data point in the macro toolkit. If they cross that threshold, I will cut equity to 60% and move the excess into 2-year Treasuries. The labor market is the only thing holding the consumer together. If it cracks, the late-cycle label becomes untenable.

-

If the VIX closes above 35.0 — that is the panic threshold. At 16.99 today, we are nowhere near it. But if it hits 35, the regime signal becomes irrelevant. I will go to 50% cash, 30% equity, 10% gold, and 10% T-bills within 24 hours. Panic is self-fulfilling in a low-confidence regime.

Levels that matter: WTI $104.28 · HY OAS 4.69% · 10Y real yield 2.3% · Weekly jobless claims 236,500 · VIX 35.0

For the full signal dashboard, allocation table, and watch list, see this week's CIO Weekly →

Get this research delivered

New analysis, directly to your inbox. Research notifications only.