Weekly Macro Report

Macro Brief — April 20, 2026

Oil's surge to $87 reveals the late-cycle economy's inflation vulnerability as tech earnings loom.

Parson Tang — April 20, 2026Powered by MARY

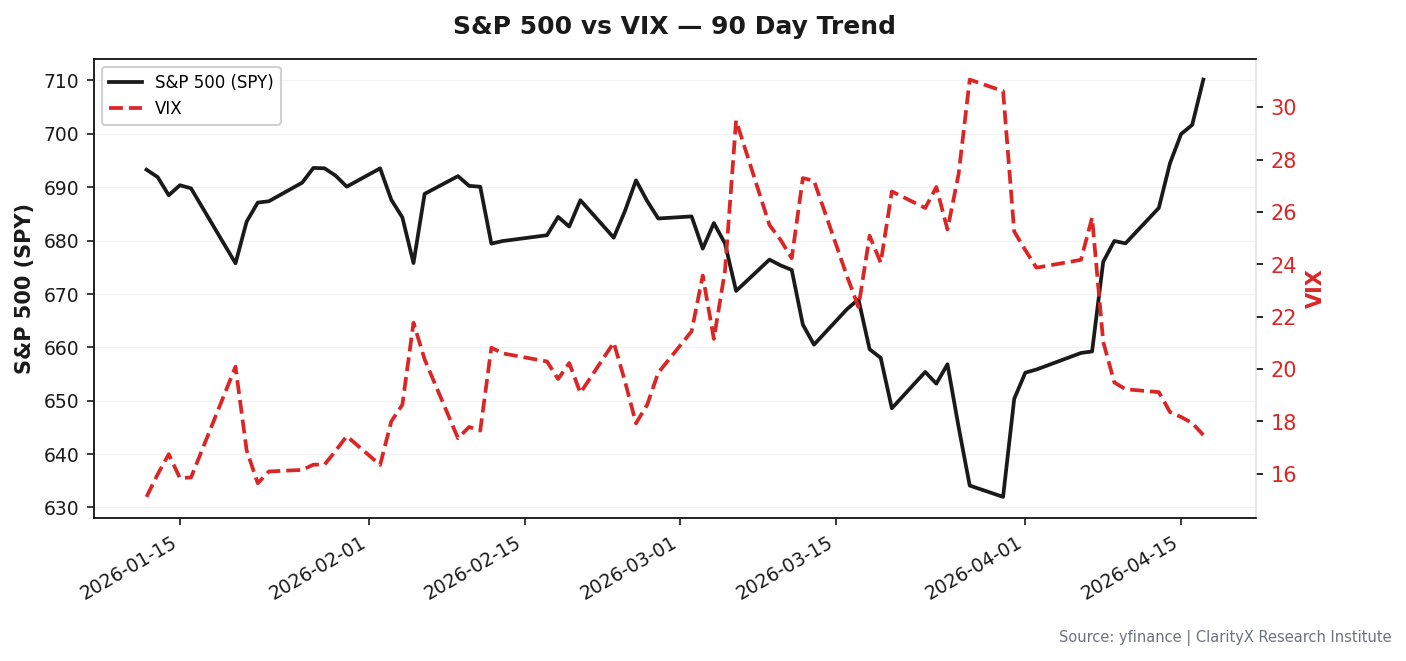

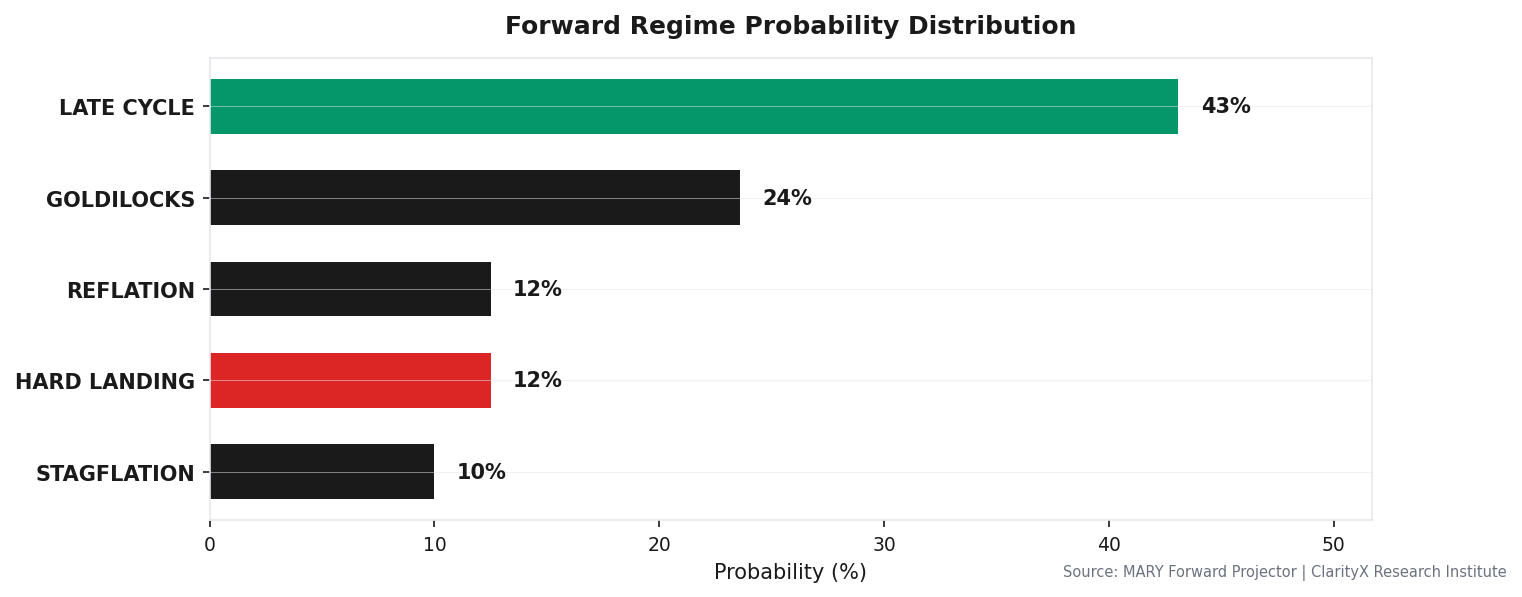

The picture is largely unchanged from last week, but the direction of the move is telling. My confidence in the Late-Cycle label ticked up from 44% to 46%. That’s not a ringing endorsement—it’s still a coin toss—but the market’s reaction to oil’s rebound is the story. WTI didn’t just stabilize; it rallied over $4 to $87.28. And the VIX drifted lower. The market is pricing the return of a known risk (higher energy prices) as less concerning than the sudden removal of an unknown one (a blocked Strait). That’s complacency, not calculation.

The Unchanged Foundation

The thesis remains intact, held together by the same fragile pillar. Growth is anemic at 0.5% GDP, but inflation expectations are anchored at 2.36% for the 5-year forward. This allows the Federal Reserve to stand pat with the Fed Funds rate at 3.64%, keeping real yields—the inflation-adjusted return on safe government bonds—contained at 2.30%. Credit spreads, the premium companies pay over Treasuries, are still tight. High-yield OAS is at 2.86%; investment-grade is at 1.01%. The financial plumbing isn’t signaling distress.

But the cost-push pressure is real and rising again. Wage growth is still running at 3.52% year-over-year. CPI, as of the last print, is 3.32%. Now oil is marching back toward $90. The consensus assumes these inputs won’t de-anchor long-term expectations. It’s a bet on Fed credibility and consumer psychology. It’s also the only thing preventing restrictive real yields from spiking and decisively ending the cycle.

The Contradiction in the Portfolio

My macro view is cautious, with less than 50% confidence in the stability of this regime. Yet the engine’s allocation sits at 77% equities. This divergence isn’t a bug; it’s a feature of late-cycle investing.

The market is telling us that without an imminent, explosive break in the labor market or the credit system, there is no forced seller. Financial conditions are still loose. The credit market is singing, not screaming. Therefore, the path of least resistance for equities is sideways to slightly up, driven by sector rotation and earnings, not macro expansion. The 77% allocation is a tactical hold in that environment, heavily biased toward the quality and sectors that perform when growth stalls but doesn’t collapse. It’s a high-wire act, but the net below—for now—is intact.

Sector Rotation

The sector leadership this week reinforces this tense equilibrium. Over the last three months, it’s not a clean signal. It’s a barbell.

On one end, you have the obvious cyclical winner: Energy (XLE), up 14.7% relative to the S&P 500, directly fueled by the oil price move. Materials are strong too. On the other end, you have defensive yield plays: Real Estate (XLRE, +5.1%) and Utilities (XLU, +4.2%) showing surprising strength despite restrictive real yields. Technology and Industrials are in the green, but in the middle of the pack.

The market is simultaneously chasing the inflation trade and hiding in rate-sensitive defensives. This is the fingerprint of allocators who are hedging their books, not committing to a direction. They’re buying both the rumor of persistent inflation and the hope that it won’t kill the cycle.

What Would Change My Mind

I am monitoring two trip wires. If either is breached, the "monitoring" stance shifts to "acting," and the 77% equity allocation gets cut.

- Credit Stress: The high-yield market is complacent at a 2.86% OAS. If high-yield spreads (OAS) sustainably break above 5.0%, it signals corporate stress is overwhelming liquidity. This would trigger an immediate 15-point reduction in equity exposure, moving to cash and long-duration Treasuries.

- Labor Fracture: The weekly jobless claims number is my canary. A print above 236,500 would be the first concrete signal the resilient labor pillar is cracking. I would interpret this as the start of a trend, reducing equity exposure by 10 points and increasing defensive sector weightings.

The yield curve remains deeply inverted, which historically screams recession. I’m discounting its signal slightly right now because term premium is distorted by the Fed’s balance sheet and global demand for safe assets. I trust the message from current growth data and credit more than the curve’s structural warning. But if my two thresholds above are hit, the curve’s message will become the primary one.

What I’m Doing

The urgency gear is set to MONITORING. We are watching the data, not reacting to it. The foundation is fragile but holding. No portfolio action is warranted this week.

- Adding to: Nothing new. The position is set.

- Avoiding: Significant new cyclical bets, especially in consumer discretionary. High-leverage, low-quality small caps are also off the menu, as their recent underperformance hints at.

- Bottom Line: The regime is unstable, but the market is paying you to wait for the break. The 77% equity allocation is a bet that the break won’t come this week, or next. It’s a tactical hold in a strategic fog. The moment the data shifts from showing cracks to falling through, we will be out the door.

Levels that matter: WTI $87.28 · 10Y Real Yield 2.30% · High-Yield Spread 2.86% · VIX 17.48

For the full signal dashboard, allocation table, and watch list, see this week's CIO Weekly →

Charts

S&P 500 vs VIX — 90 Day Trend

S&P 500 vs VIX — 90 Day Trend

Forward Regime Probability Distribution

Forward Regime Probability Distribution

Get this research delivered

New analysis, directly to your inbox. Research notifications only.