Weekly Macro Report

Macro Brief — April 17, 2026

Oil's $7 plunge signals a recession bet the stock market refuses to make.

Parson Tang — April 17, 2026Powered by MARY

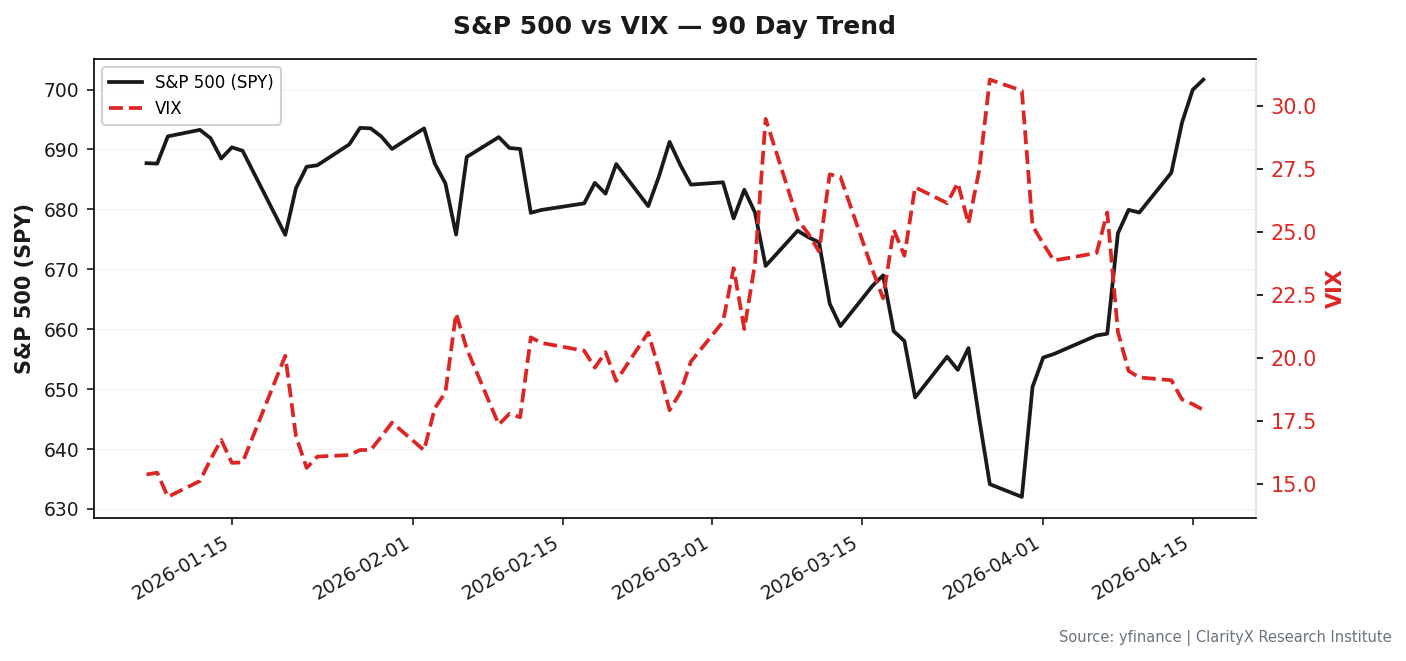

The Strait of Hormuz is open. Oil is back at $83. The market is breathing a sigh of relief, and the VIX is drifting lower. The 28% probability of a liquidity crisis I flagged two weeks ago has evaporated.

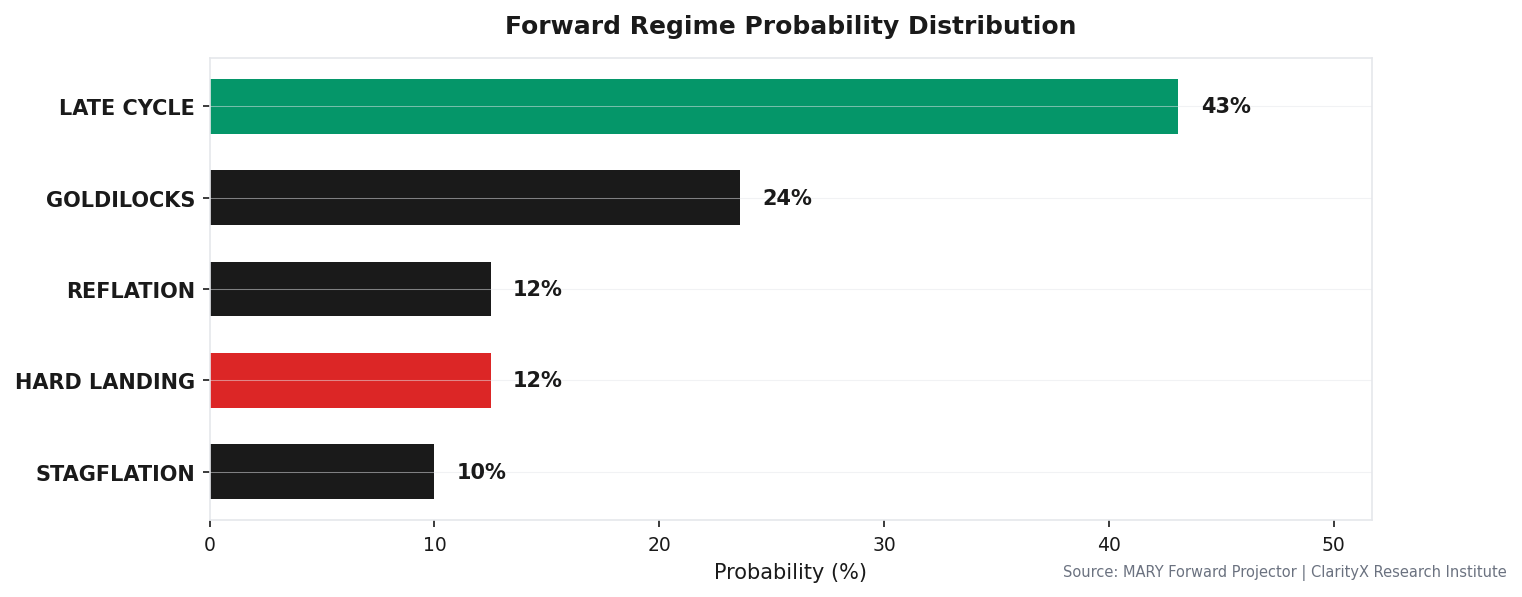

But the regime hasn’t changed. We’re still in Late-Cycle, with my confidence in that label now at 44%. The oil shock was averted, and the stance is unchanged: hold 78% in equities, keep the 7% cash reserved for a specific crisis signal, watch the two trip wires. The market is mistaking the removal of an acute geopolitical threat for a reason to reposition. It isn’t.

The Fragile Foundation

The thesis holding this late-cycle together is simple: anchored inflation expectations keep real yields from spiking and crushing equity multiples. Last week, with oil at $111, that anchor was being tested. This week, with oil down $28, the anchor feels secure again. The Michigan survey’s 5-year inflation expectation is steady at 3.4%.

But look at the other side of the equation: growth. GDP is running at a paltry 0.5%. Housing permits are weakening. The only thing preventing this from tipping into a more dangerous regime is a resilient labor market, with jobless claims holding around 210,000. The consensus assumes this stability persists, allowing the Federal Reserve to stay neutral with the Fed Funds rate at 3.64%.

This is the fragile pillar. The entire construct rests on the labor market not breaking. If jobless claims begin a sustained climb toward 300,000, the Fed’ neutral stance would be challenged, real yields—currently at 2.30%—could become volatile, and those tight credit spreads would finally start to widen. The relief rally we’re seeing is in the price of oil, not in a fundamental improvement in growth.

The Contradiction in the Portfolio

Here’s the operational tension. My macro view is cautious, with regime confidence below 50%. Yet the portfolio allocation from our engine sits at 78% equities. This isn’t a blind contradiction; it’s a calculated position.

The market is telling us that without an imminent oil-driven inflation spike, there’s no immediate catalyst to break the cycle. Financial conditions, as measured by the Chicago Fed’s National Financial Conditions Index (NFCI), are still accommodative at -0.465. High-yield bond spreads—the premium risky companies pay to borrow—are tight at 2.85%. Investment-grade spreads are at a mere 1.01%. The credit market is not signaling distress.

So we’re positioned for resilience, not for recession. The 78% equity allocation is heavily tilted toward quality and sectors that can weather a stagnant, late-cycle environment. It’s a high-conviction allocation to a low-conviction regime.

Sector Rotation

The sector leadership confirms this messy, transitional state. We’re not seeing a clean “risk-on” or “risk-off” signal. Instead, it’s a split personality.

The top performers over the last three months are Energy (XLE, +12% relative strength) and defensive yield plays like Real Estate and Utilities. At the same time, Technology and Industrials are also showing strength. The market is simultaneously betting on the energy trade’s cash flows and hiding in defensives, while still granting a bid to growth. This is the fingerprint of a market that doesn’t know what’s next but is willing to pay for both protection and participation.

What Would Change My Mind

My cautious view is contingent on the stability of two things: labor and credit. If either cracks, the allocation changes immediately.

- Labor Deterioration: Weekly jobless claims above 236,500. That number is the engine's calibrated threshold — not 250k, not a 4-week average. A print above it is the first signal the resilient labor pillar is cracking. Action: trim equity by 5 percentage points, add to cash.

- Credit Event: High-yield option-adjusted spread widens above 5.0% — from 2.85% today. At that level, the corporate credit market is pricing real default risk, not just volatility. Action: cut equity to crisis allocation, move to cash and short-duration Treasuries.

- VIX Panic: VIX above 35 for 3 consecutive days signals a dislocation, not just noise. This is the trigger for deploying the 7% cash reserve into broad equity — buying the panic, not fleeing it.

What I’m Doing

The urgency this week is MONITORING. The immediate fire is out, so we are watching the data, not reacting to it.

Adding / Overweight:

- Quality Mega-Caps & Healthcare: This is the core of the 78% equity stake. We’re favoring companies with fortress balance sheets and non-cyclical earnings.

- Energy (XLE): Maintaining an overweight. The sector has given back some gains but remains a source of cash flow and a hedge against geopolitical recurrence. The $28 oil drop is a gift for rebuilding the position.

Avoiding / Underweight:

- Long Duration Bonds: Real yields at 2.30% in a stagnant growth environment offer poor compensation and are vulnerable if growth surprises to the upside.

- Low-Quality Cyclicals: There is no margin of safety in highly leveraged companies in discretionary consumer or industrial sectors.

- Broad High-Yield Credit: A 2.85% spread does not pay you for the late-cycle risk.

The bottom line: we dodged a bullet, not the regime. But the action is clear — hold quality, stay at 78% equity, keep the dry powder loaded, and wait for the data to give a signal before moving. Late Cycle historically runs 12–24 months. War doesn’t break cycles — credit does. At 2.85%, the credit market is calm. Until that changes, the position doesn’t.

Levels that matter: S&P 500 5521 · WTI $83.24 · 10Y Real Yield 2.30% · High-Yield Spread 2.85% · VIX 17.94

For the full signal dashboard, allocation table, and watch list, see this week's CIO Weekly →

Charts

S&P 500 vs VIX — 90 Day Trend

S&P 500 vs VIX — 90 Day Trend

Forward Regime Probability Distribution

Forward Regime Probability Distribution

Get this research delivered

New analysis, directly to your inbox. Research notifications only.